How Sellers Maximize HDB Sale Proceeds in 2026

- Pallipallisell

- Jun 12

- 9 min read

Maximizing HDB sale proceeds is defined as the process of increasing your net cash-in-hand after deducting all costs from the gross sale price, including CPF refund obligations, outstanding loans, agent commissions, and legal fees. Most sellers focus on the headline price and miss the real number that matters. Understanding how sellers maximize HDB sale proceeds requires you to control four levers: strategic pricing, transaction cost reduction, CPF planning, and cash flow timing. Get all four right, and you keep significantly more of what your flat is actually worth.

How do pricing strategies influence your HDB sale proceeds?

Pricing is the single most powerful lever for maximizing net proceeds. Set it wrong, and you either leave money on the table or sit on the market for months while your costs accumulate.

The standard method is to price based on the median of the last 10 comparable transactions within 500 meters of your flat, filtered by floor level, flat type, and remaining lease. This gives you a defensible anchor. From there, you adjust up or down based on your flat’s condition, floor level, and the current buyer pool under the Ethnic Integration Policy (EIP). The EIP limits which buyers can purchase your flat based on ethnic quotas, which directly shrinks your addressable market and can affect how aggressively you price.

Pricing 8-10% below the median secures offers in under two weeks with over 90% probability, but it risks leaving $30,000 to $50,000 on the table for a typical 4-room flat. That is a significant sacrifice for speed. On the other end, pricing 5% above median can work in a tight supply market, but overpricing by 5% doubles your average days on market and reduces the probability of a clean sale.

Pricing Strategy | Effect on Days on Market | Effect on Net Proceeds |

8-10% below median | Under 2 weeks | $30,000-$50,000 lower |

At median | 4-6 weeks typical | Balanced outcome |

5% above median | Doubles average timeline | Potentially higher, higher risk |

Pro Tip: If you receive eight or more viewings with no offers within four weeks, the problem is almost certainly your price, not your listing. Drop 3-5% and reassess. Learn how to read these signals with a proper HDB pricing guide before you list.

The typical listing-to-handover timeline is 10 to 12 weeks when priced correctly. Overpricing stretches this timeline and increases your holding costs, which quietly erodes your net proceeds even if you eventually close at your asking price.

What are the main transaction costs that reduce your net proceeds?

Transaction costs are the most controllable deduction in your sale. Unlike CPF obligations or outstanding loans, you have real choices here.

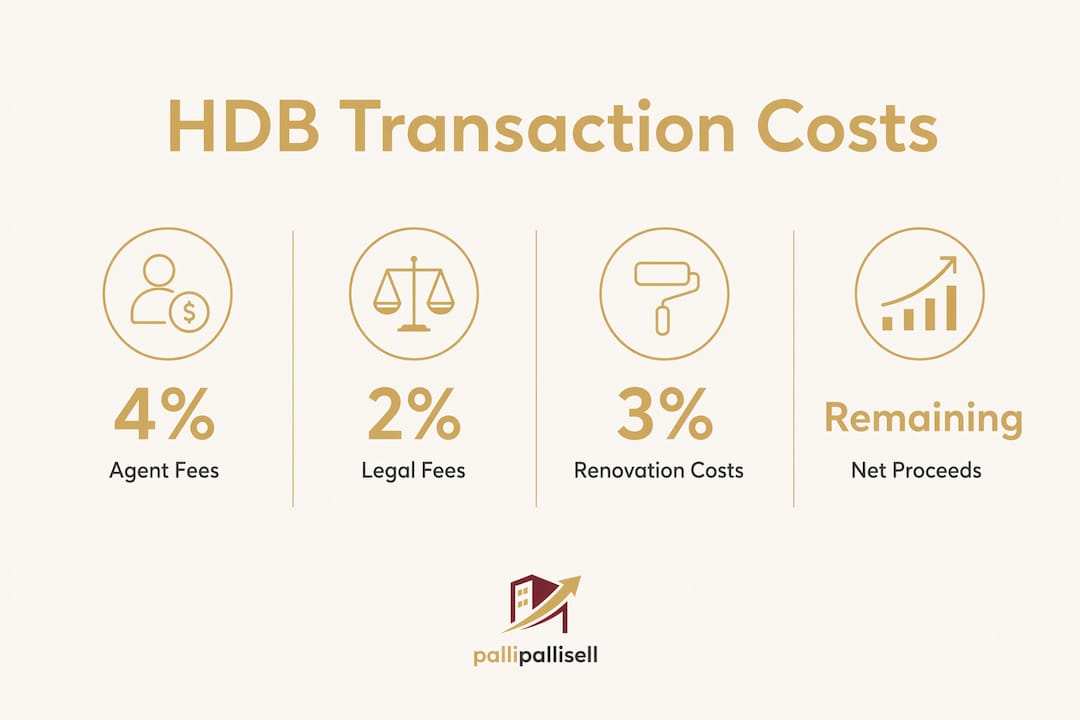

Agent commissions range from 1% to 3% of the sale price. On a $680,000 HDB flat, that is $6,800 to $20,400 gone before you see a dollar. Legal and conveyancing fees add another $1,800 to $5,000. HDB administrative fees and miscellaneous costs layer on top. The total friction from these costs can consume 3% to 5% of your gross sale price.

Here is where you can act:

Skip or reduce agent commission. Self-managed sale platforms charge a flat fee instead of a percentage. Pallipallisell charges $688, compared to $13,600 or more on a $680,000 sale with a traditional agent. That gap is real cash you keep.

Shop legal fees. Conveyancing rates are not fixed. Get quotes from at least three law firms. Fees vary by $1,000 or more for identical work.

Understand HDB admin fees upfront. HDB charges resale application fees of $40 for the first room and $50 per additional room. These are fixed and non-negotiable, but knowing them prevents surprises.

Avoid unnecessary add-ons. Some agents bundle staging, photography, and marketing into their commission. You can source these separately for a fraction of the cost.

Pro Tip: Sellers who sell HDB without an agent and use a fixed-fee platform retain the full commission saving. On a $700,000 flat, that is $7,000 to $21,000 back in your pocket.

The net cash-in-hand after a typical HDB sale ranges from 40% to 60% of the sale price after all deductions. A 4-room flat sold at $580,000 can yield net proceeds of around $200,920. Cutting transaction costs is the fastest way to push that number higher without changing your asking price.

How does CPF refund and accrued interest affect your actual cash-in-hand?

CPF refund is the most underestimated deduction in any HDB sale. Many sellers calculate their expected cash proceeds without accounting for it fully, then face a shock at completion.

Here is how it works:

When you used CPF Ordinary Account (OA) funds to pay for your flat, those funds must be refunded to your CPF account upon sale.

The refund is not just the principal you withdrew. It includes 2.5% compounded accrued interest for every year the money was out of your CPF account.

On a flat owned for 11 years with $420,000 in CPF used, the accrued interest alone reaches approximately $131,000. That is $131,000 that goes back to CPF, not to your bank account.

The refunded amount sits in your CPF OA and can be used for your next property purchase, but it is not liquid cash.

Many sellers treat the CPF refund as “lost money.” It is not. The funds return to your CPF account and remain available for your next property purchase or retirement. The real issue is that it reduces your immediate cash proceeds, which affects your ability to fund a simultaneous upgrade without a bridging loan.

The practical implication: calculate your CPF refund obligation before you commit to any purchase timeline. Use the CPF Board’s online calculator or request a projection from HDB. If your accrued interest is large, your cash-in-hand after sale may be far lower than your gross sale price suggests. This is especially critical for upgraders who plan to use cash proceeds to fund the gap on a new property.

Should you renovate your HDB before sale to increase proceeds?

Renovation before sale is one of the most debated strategies for HDB sellers. The honest answer is that it rarely delivers the return sellers expect.

Renovation investments above $30,000 to $42,000 typically yield diminishing returns. Beyond that threshold, each additional dollar spent on renovation adds only marginal value to your resale price. The areas with the highest buyer impact are kitchens, bathrooms, and flooring. These are the spaces buyers inspect most closely and where dated finishes create the strongest negative impression.

Renovation does not guarantee higher sale prices. Market timing, location, and competitive supply matter more. A well-priced unrenovated flat in a sought-after block will outsell an over-renovated flat in a less desirable location every time.

Before committing to any renovation spend, ask yourself these questions:

Can you recover the renovation cost in the sale price, given recent comparable transactions in your block?

Do you have the time? A full renovation takes 6 to 10 weeks, which delays your listing and extends your holding period.

Is your flat already priced at a premium? If so, buyers already expect a certain standard. If not, a basic refresh may be more cost-effective.

Pro Tip: Professional staging and quality photography cost $500 to $2,000 combined and consistently improve buyer first impressions. This is a far better return than a $15,000 kitchen overhaul on a flat you are selling within six months.

The smarter play for most sellers is to fix obvious defects, repaint in neutral tones, declutter thoroughly, and invest in professional photos. This approach costs under $3,000 and positions your flat competitively without the financial risk of a full renovation.

What timing and cash flow strategies help maximize your HDB sale proceeds?

Timing your HDB sale correctly protects your net proceeds just as much as pricing does. Poor sequencing creates cash flow gaps that force you into expensive bridging loans or rushed decisions.

The two main paths for upgraders are sell-then-buy and buy-then-sell. Each carries distinct risks:

Sell-then-buy: You sell your HDB first, collect proceeds, then purchase your next property. This eliminates bridging loan risk and gives you a clear cash position. The downside is a potential gap period where you need temporary housing.

Buy-then-sell: You secure your new property first, then sell your HDB. This avoids the housing gap but exposes you to cash flow shortfalls during the 3 to 6 month overlap between paying for the new property and receiving HDB sale proceeds.

Most upgrade failures occur because sellers underfund this 3 to 6 month cash flow gap, leading to bridging loan dependency and higher interest costs. Map this timeline before you sign any Option to Purchase.

Additional timing considerations:

ABSD remission: Singapore citizens who own an HDB and purchase a private property must pay Additional Buyer’s Stamp Duty (ABSD) upfront, but can apply for remission if they sell their HDB within six months of the new property’s purchase. Missing this window costs you a significant sum.

TDSR compliance: Outstanding HDB mortgages affect your Total Debt Servicing Ratio, which can cause loan application failures for your upgrade. Redeem your HDB loan before exercising the new property’s Option to Purchase, or disclose it clearly if taking the buy-then-sell path.

Completion alignment: Coordinate your HDB completion date with your new property’s key collection date to minimize the cash gap and avoid paying rent while waiting for proceeds.

Pro Tip: Build a simple spreadsheet that maps your HDB sale completion date, CPF refund amount, net cash proceeds, new property payment schedule, and ABSD remission deadline. Seeing all four numbers together prevents the most common and costly upgrader mistakes.

Key takeaways

Sellers who maximize HDB sale proceeds control four variables: asking price relative to comparable transactions, transaction costs through low-fee or self-managed options, CPF accrued interest obligations calculated before committing to a timeline, and cash flow sequencing to avoid bridging loans and ABSD penalties.

Point | Details |

Price at median, not above | Overpricing by 5% doubles days on market and reduces sale certainty. |

Cut transaction costs first | Switching to a fixed-fee platform saves $7,000-$20,000 compared to traditional agent commissions. |

Calculate CPF refund early | Accrued interest at 2.5% compounded can add over $131,000 to your refund obligation on a long-held flat. |

Limit renovation spend | Renovation above $30,000-$42,000 rarely recovers its cost; staging and photography deliver better ROI. |

Map your cash flow timeline | The 3-6 month gap between new property payment and HDB proceeds is the most common upgrader cash trap. |

What I’ve learned from watching sellers get this wrong

I have seen sellers walk away from their HDB sale with far less than they expected, and the pattern is almost always the same. They fixated on the gross sale price and ignored the four deductions that actually determine their cash position.

The CPF accrued interest calculation is the one that surprises people most. A seller who used $420,000 in CPF over 11 years and expects to pocket a large portion of their $800,000 sale price can be genuinely shocked when $550,000 or more is absorbed by loan repayment, CPF refund, and fees. Run this number before you list, not after you accept an offer.

On pricing, the temptation to push 5% to 10% above median is understandable. Your flat has sentimental value and you know what you put into it. But buyers do not pay for your memories. They pay for what comparable flats sold for last quarter. Price at or just below median, generate competition, and let multiple offers push the price up naturally. That is how you get a premium, not by starting there.

The renovation trap is real. I have watched sellers spend $40,000 on a full renovation expecting to add $60,000 to their sale price, only to find that buyers in their block simply do not pay that premium. Spend $2,000 on staging and photography instead. The return is measurably better.

Finally, if you are upgrading, treat the cash flow timeline as seriously as you treat the sale price. The sellers who end up in bridging loans are not unlucky. They are the ones who did not model the gap.

— Brandon

Sell your HDB for more with Pallipallisell

Pallipallisell is built for sellers who want to keep more of their sale proceeds. Instead of paying 1% to 3% in agent commissions, you pay a flat fee of $688 and manage your sale directly. On a $700,000 HDB flat, that is up to $20,400 saved before you even negotiate your price. The platform gives you full control over your listing, buyer communications, and closing process. Explore affordable selling options and see exactly what you save, or go straight to the self-managed sale service to get started today.

FAQ

What does “net HDB sale proceeds” actually mean?

Net HDB sale proceeds are the cash you receive after deducting outstanding loan repayment, CPF principal and accrued interest refund, agent commissions, legal fees, and HDB admin fees from your gross sale price. Net proceeds typically range from 40% to 60% of the sale price.

How much can I save by not using a traditional agent?

Agent commissions range from 1% to 3% of the sale price, which equals $6,800 to $20,400 on a $680,000 flat. Using a fixed-fee platform like Pallipallisell at $688 saves you the full commission amount.

Does renovating my HDB before selling increase my sale price?

Not reliably. Renovation above $30,000 to $42,000 yields diminishing returns, and market timing and location have more influence on price than renovation quality.

What is CPF accrued interest and why does it matter?

CPF accrued interest is the 2.5% compounded annual interest on CPF funds you used to purchase your flat, which must be refunded to your CPF account upon sale. On a flat held for 11 years with $420,000 in CPF used, this accrued interest reaches approximately $131,000, directly reducing your available cash proceeds.

What is the fastest way to sell my HDB at a good price?

Price at the median of the last 10 comparable transactions within 500 meters, invest in professional photography, and list on high-traffic platforms. The typical listing-to-completion timeline is 10 to 12 weeks when priced correctly.

Recommended

Comments