HDB vs Private Property Sale Differences in Singapore

- Pallipallisell

- Jun 19

- 7 min read

Selling a property in Singapore means navigating two very different systems. The HDB vs private property sale differences go far beyond price. HDB flats operate under government rules, including Minimum Occupation Periods (MOP), resale restrictions, and fixed procedures through the HDB Resale Portal. Private properties follow open market rules with negotiable terms, broader buyer pools, and potential Seller’s Stamp Duty (SSD) obligations. Your costs, timelines, and net proceeds depend entirely on which category your property falls under. Understanding both systems before you list is the single most important step you can take.

What are the main cost differences between selling HDB and private property?

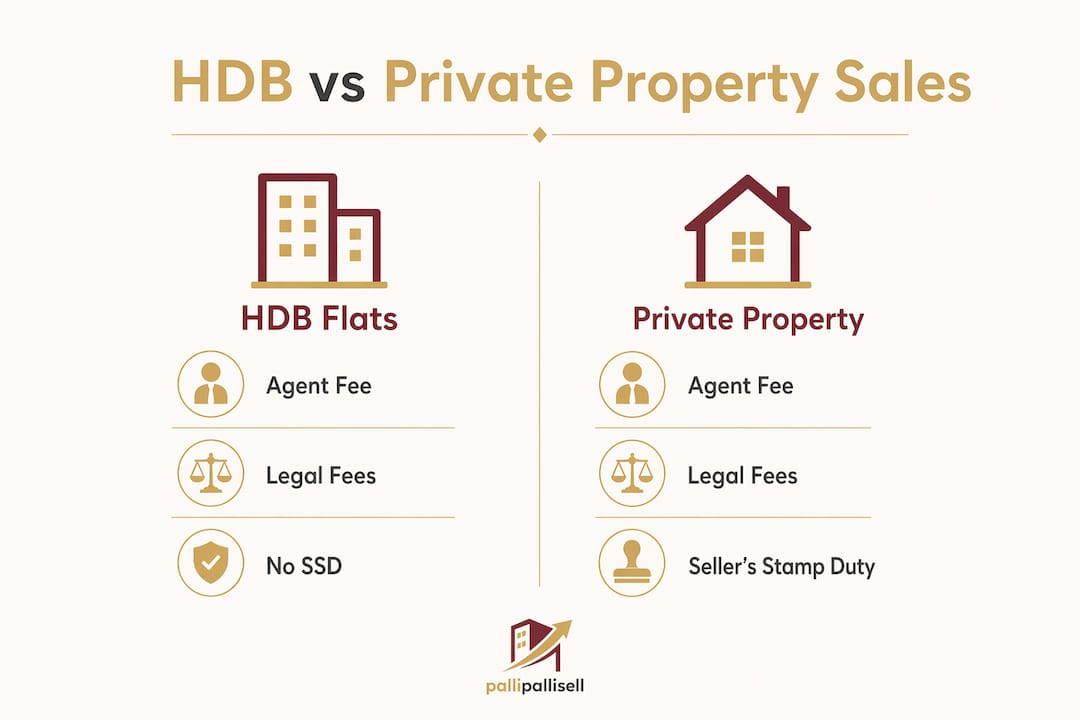

Agent commissions are typically around 2% for HDB resale flats and 1–2% for private properties in Singapore. That gap matters on a $600,000 HDB flat. A 2% commission equals $12,000 out of your pocket before any other fees.

Legal fees add another layer. HDB legal fees generally range from $2,500 to $5,000. Private property sellers face varied legal costs that can run higher, especially when mortgage discharge and CPF refund coordination are involved.

The biggest cost difference is the Seller’s Stamp Duty. Private property sellers pay SSD up to 16% if they sell within four years of purchase. HDB sellers pay no SSD at all. Selling a $1.2 million private property within year one could cost you $192,000 in SSD alone.

Here is a direct comparison of the key selling costs:

Cost Item | HDB Flat | Private Property |

Agent commission | ~2% of sale price | 1–2% of sale price |

Legal fees | $2,500–$5,000 | Varies, often higher |

Seller’s Stamp Duty | None | Up to 16% within 4 years |

Maintenance arrears | Minimal | Higher monthly fees possible |

HDB Resale Portal fee | Small admin fee | Not applicable |

Pro Tip: Commission is negotiable, even for HDB sales. Always confirm the agreed rate in writing before signing any agent appointment. Better yet, explore fixed-fee platforms like Pallipallisell to avoid percentage-based commissions entirely.

How do timelines and procedures differ for HDB vs private property sales?

The HDB sale process is structured and government-managed. The HDB Resale Portal controls submissions, acknowledgments, and approvals. Private property sales are more flexible but involve more legal coordination between lawyers, banks, and buyers.

The most critical timeline factor for HDB sellers is the MOP. HDB flats require a 5-year MOP before you can sell on the resale market. Prime and Plus flat owners face a 10-year MOP. Private properties carry no MOP at all. You can sell a private condo the day after you buy it, though SSD will apply if you do so within four years.

Once you are eligible to sell, here is how the typical process unfolds for each property type:

HDB resale sale steps:

Confirm MOP eligibility through the HDB Resale Portal

Grant the buyer an Option to Purchase (OTP) with a fixed 21-day exercise window

Both parties submit resale applications through the HDB Resale Portal

HDB reviews and issues an acknowledgment letter

Complete the resale transaction, typically within 8 weeks of acknowledgment

Private property sale steps:

Appoint a lawyer and confirm mortgage discharge terms

Grant the buyer an OTP, typically with a 14-day exercise window

Buyer exercises OTP and signs the Sale and Purchase Agreement

Lawyers coordinate title transfer, CPF refund, and mortgage discharge

Complete the transaction, typically within 10–12 weeks of OTP exercise

Private property transactions require careful timeline coordination between lawyers, banks, and CPF. That extra coordination is why private sales take longer than HDB resales.

Pro Tip: If you are selling HDB and buying private simultaneously, plan your HDB completion date first. Your CPF refund from the HDB sale affects how much cash you have available for the private property downpayment.

What strategic advantages and constraints should you consider?

The differences in home sale strategy between HDB and private property go well beyond fees and timelines. Your buyer pool, subsidy obligations, and financing options all shift depending on which type you own.

HDB sellers face a narrower buyer pool by design. Prime and Plus HDB flats carry resale restrictions including income ceilings for buyers, subsidy clawback, and proximity rules. Subsidy clawback means the government recovers a portion of the housing grant you received when you first bought. That amount comes directly off your net proceeds. A seller who received a $80,000 grant may see a significant portion clawed back at resale, reducing the actual cash they walk away with.

Private properties attract a broader buyer pool. Singaporeans, permanent residents, and foreigners can all buy private property. That wider pool supports stronger demand and more competitive offers. However, private condos carry higher monthly maintenance fees and SSD obligations when sold early. Those costs eat into the flexibility advantage.

Financing constraints also differ. HDB loans allow higher loan-to-value ratios and lower downpayments than private property bank loans, which operate under stricter Total Debt Servicing Ratio (TDSR) rules. When you sell your HDB and upgrade to private, your financing environment changes completely.

“HDB suits those prioritizing stability and subsidies, while private properties appeal to investors valuing flexibility and market-driven pricing.” — Market expert Alvin Tan, as cited by new-condo-launch.sg

That distinction matters for your sale strategy. If your buyer is an investor, private property is the more natural fit. If your buyer is a young family seeking stability, HDB resale value often holds up well in mature estates.

How do post-sale obligations differ between HDB and private property?

Post-sale obligations are where many sellers get caught off guard. The rules for what you must do after selling, and what you are allowed to buy next, differ sharply between the two property types.

Key post-sale obligations for HDB sellers:

HDB owners must sell their flat before purchasing private property to comply with ownership rules

All co-applicants, including your spouse and any listed occupiers, must be included in the resale submission

CPF funds used for the flat must be refunded to your CPF Ordinary Account with accrued interest upon sale

If you received a housing grant, subsidy clawback applies at the point of resale for Prime and Plus flats

Key post-sale obligations for private property sellers:

Check your mortgage for lock-in periods. Breaking a lock-in early typically triggers a penalty of 1–1.5% of the outstanding loan

Confirm your CPF refund timeline with your lawyer. CPF funds must be returned before the sale proceeds are released to you

If you plan to buy another property, calculate your Additional Buyer’s Stamp Duty (ABSD) exposure before committing

Pro Tip: Request a CPF withdrawal statement before you list your property. Knowing your exact CPF refund amount helps you calculate your actual cash proceeds accurately, so you can plan your next purchase without surprises.

Key takeaways

Selling an HDB flat and selling a private property are two fundamentally different processes, and your net proceeds depend on understanding the costs, timelines, and obligations specific to your property type.

Point | Details |

Cost gap is significant | HDB has no SSD; private property SSD can reach 16% if sold within 4 years. |

Timelines vary by type | HDB resale completes in about 8 weeks; private property takes 10–12 weeks after OTP. |

MOP restricts HDB sellers | HDB requires a 5-year MOP, or 10 years for Prime/Plus flats, before you can sell. |

Subsidy clawback reduces net proceeds | Prime/Plus HDB sellers lose a portion of grant money at resale, reducing actual cash received. |

Buyer pool affects demand | Private properties attract a broader buyer pool, including foreign buyers, supporting stronger competition. |

Why the upgrade decision deserves more scrutiny than most sellers give it

I have seen sellers rush the HDB-to-private upgrade without running the real numbers. The sticker price on a private property looks achievable until you factor in ABSD, higher monthly fees, stricter loan limits, and the loss of CPF flexibility. The financial picture changes fast.

Industry analyst Winfred Quek makes a point I find consistently accurate: upgrading from HDB to private often reflects lifestyle choices rather than financial optimization. Some households are genuinely better off staying in their HDB flat and investing the difference. That is not a popular opinion in a market where private property carries social status, but the math supports it in more cases than sellers admit.

The subsidy clawback issue is the most underestimated trap I see. Sellers of Prime and Plus flats calculate their net proceeds based on the sale price, then discover at closing that clawback reduces net proceeds by tens of thousands of dollars. That gap can derail a simultaneous private property purchase if you have not planned for it.

My honest advice: calculate your net proceeds after CPF refund, clawback, agent fees, and legal costs before you commit to any next purchase. The number you walk away with is rarely the number on the sales agreement.

— Brandon

How Pallipallisell helps you sell smarter and keep more proceeds

Whether you are selling an HDB flat or a private property, the cost of selling matters as much as the sale price. Pallipallisell gives Singapore sellers a direct, low-cost alternative to traditional agent commissions.

Instead of paying 1–2% in agent fees, Pallipallisell charges a flat fee of $688. On a $700,000 HDB flat, that saves you up to $13,300 compared to a standard 2% commission. The platform lets you list your property, communicate directly with buyers, and manage the entire sale process yourself. You stay in control. You keep more of your proceeds. Check out Pallipallisell’s affordable selling plans and browse current property listings to see how other Singapore sellers are making the move.

FAQ

What is the MOP for HDB flats before selling?

The standard MOP for HDB flats is 5 years from the date of key collection. Prime and Plus flat owners must wait 10 years before selling on the resale market.

Does selling an HDB flat incur Seller’s Stamp Duty?

No. HDB sellers do not pay SSD. SSD applies only to private property sellers who sell within 4 years of purchase, at rates up to 16%.

How long does an HDB resale transaction take to complete?

HDB resale transactions typically complete within 8 weeks after HDB issues the acknowledgment letter. Private property sales take 10–12 weeks after the buyer exercises the Option to Purchase.

Can I own both an HDB flat and a private property at the same time?

Generally, no. HDB regulations require owners to dispose of their HDB flat before purchasing private property to avoid multi-property ownership conflicts.

Are agent commissions negotiable for HDB and private property sales?

Yes. Commissions are negotiable for both property types. The market standard is around 2% for HDB and 1–2% for private property, but fixed-fee arrangements are available through platforms like Pallipallisell.

Recommended

Comments